RERA Act

RERA Act Maharashtra

Maharashtra

Karnataka

Karnataka

Telangana

Telangana

Andhra Pradesh

Andhra Pradesh

Delhi

Delhi

Uttar Pradesh

Uttar Pradesh

Haryana

Haryana

Gujarat

Gujarat

Bihar

Bihar

How to increase your CIBIL Score?

- Friday 31st May 2019

- Author: Shreya Uppal

Highlights

Many of you have heard of terms like CIBIL Score, Credit score and Credit Report. When an individual or a company apply for a loan then his assessment is primarily done on the CIBIL score he has obtained.

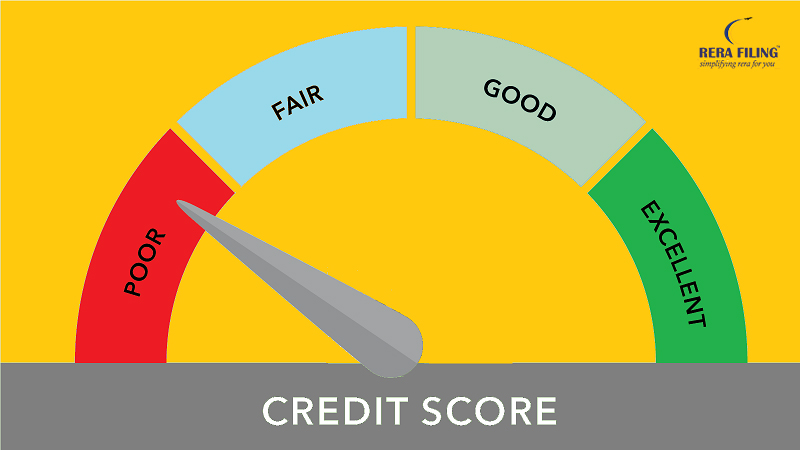

Credit score refers to a 3 digit numeric value which represents the creditworthiness of an individual. The creditworthiness ranges between 300 to 900 with 900 being the highest and 300 being the least. This score is computed with the help of the credit history of an individual.

Many of you have heard of terms like CIBIL Score, Credit score and Credit Report. When an individual or a company apply for a loan then his assessment is primarily done on the CIBIL score he has obtained. With the sole purpose to help with you these similar terms some of the points have been highlighted below:

What is CIBIL?

The Credit Information Bureau (India) Limited or CIBIL is a credit information repository. Its aim is to help its members such as lenders and credit card providers take better lending and approval decisions. In other words, it helps its members give loans and credit cards to people with decent credit history.

What is Credit Score offered by CIBIL?

Credit score refers to a 3 digit numeric value which represents the creditworthiness of an individual. The creditworthiness ranges between 300 to 900 with 900 being the highest and 300 being the least. This score is computed with the help of the credit history of an individual. Banks and most of the financial institutions prefer extending credit to an individual whose score is 750 and more. Individuals with good credit scores are less likely to default on their loan payments.

Even if you have scored less than 750, don’t get disheartened, there are few effective ways that can help you improve your CIBIL Score:

1. Be Disciplined with Repayments

Nothing damages your credit score more than delayed payments and outstanding debt. If you use credit cards or have taken a loan, ensure that you pay the credit card bills and loan EMIs on time. Delays in EMI payments not only force you to pay a penalty but also lower your credit score. So, if you find that this is something that you’re guilty of, make it a point to set reminders for EMI payments so that you can tackle them on time.

2. Borrow according to your Repaying capacity

One of the best ways to improve the CIBIL score is to borrow only what you can repay. Taking a loan is now easier than ever. But while loans are now easily available, you should never borrow more than you need. The higher the borrowed amount is, the higher will be the EMI and the higher will be the chances of missing payments. Your credit utilization ratio has a significant impact on your credit score. The more you are able to restrict your credit usage as per the allotted limit, the better it is for your credit score. Reaching the limit has the opposite effect as it lowers your credit score. One way of tackling this is to get in touch with your lender and customize your credit limit based on your expenses.

3. Using your Credit cards wisely

The habit of impulsive buying must be controlled. One should know the boundary line of everything and Excess of anything is bad. So, use your credit cards wisely. Use it where you cannot avoid because at the end of the month you will pile up so much interest cost which will become a burden in the near future. Also, try to pay credit card bills in full rather than only making the minimum payment.

4. Handle Loan rejections smartly

If you are looking for ways to increase the CIBIL score, you should also handle a loan or credit card rejections with care. While CIBIL only maintains your credit information, banks and credit card providers can see how many times your report has been accessed by other loan and credit card providers. Multiple applications within a short span of time demonstrate a credit-hungry behavior and can affect your creditworthiness. So, when applying for a new loan or credit card make sure that you first check the eligibility requirements of the provider. Be patient if your application is rejected and avoid multiple applications within a short span of time.

5. Opt for Longer Tenure while taking a loan

While borrowing a loan, try choosing a longer tenure for repayment. This will ensure that your EMI is low, and so, you are able to make payments on time. When you don’t default, delay or skip paying EMIs, your credit score will improve.

6. Avoid taking too much debt at one time

The number of loans you take in a fixed period of time should be minimal. Repay one loan and then take another to keep your credit score from crashing. If you take multiple loans at once, it will show that you are in an unforgiving cycle where you have insufficient funds. As a result, your credit score will fall further. On the other hand, if you take a loan and repay it successfully, it will give your credit score a boost.

7. Check your CIBIL Report

While the chances are rare, but it is possible for your CIBIL report to have errors. For instance, your bank might have failed to inform CIBIL that you have recently repaid a loan or paid the credit card bills in full. So, ensure that you check your CIBIL Report from time to time. This will help you identify any errors and correct them by submitting a CIBIL Dispute Resolution Form online. As a result, your credit score will improve.

More Articles

- Online Listing Tips for Real Estate Agents

- How to start a Real Estate business in India - a complete guide !

- Renting Vs Buying property - How will you decide?

- What you should do in Property Management services

- Home Loan Insurance

- How to choose your builder?

- How to ensure fire safety in your home!

- Tips To Keep In Mind While Taking A Home On Rent

- Importance of Home Security

- How to plan your property budget?

- Leased vs. Purchased vs. Co-Working Office Spaces

- Easy Tips to Build an Eco Friendly Home

- Sample Flat - A Trick by a Builder?

- How to have a Beautiful Guest Room? Impress your Guests with these Guest Room Ideas..

- Understanding MCLR and its Effects on Home Loans

- 5 simple ways to close a real estate deal

- Is it worth to buy property near an airport ?

- Home loan tax benefit

- How to be successful in business as an introvert

- Cost effective home decor ideas

- What to Be-Paying Guest or a Tenant??

- Complete guide to start your small business

- Sports township- New trend in India

- Online Listing Tips for Real Estate Agents

- Understanding Floor Area Ratio- FAR

- Town and Country Planning | Meaning and Importance

- Checklist of Important Property Documents- All You Need to Know

- Role of CREDAI in real estate

Copyright © 2026 RERA Filing. All rights reserved.