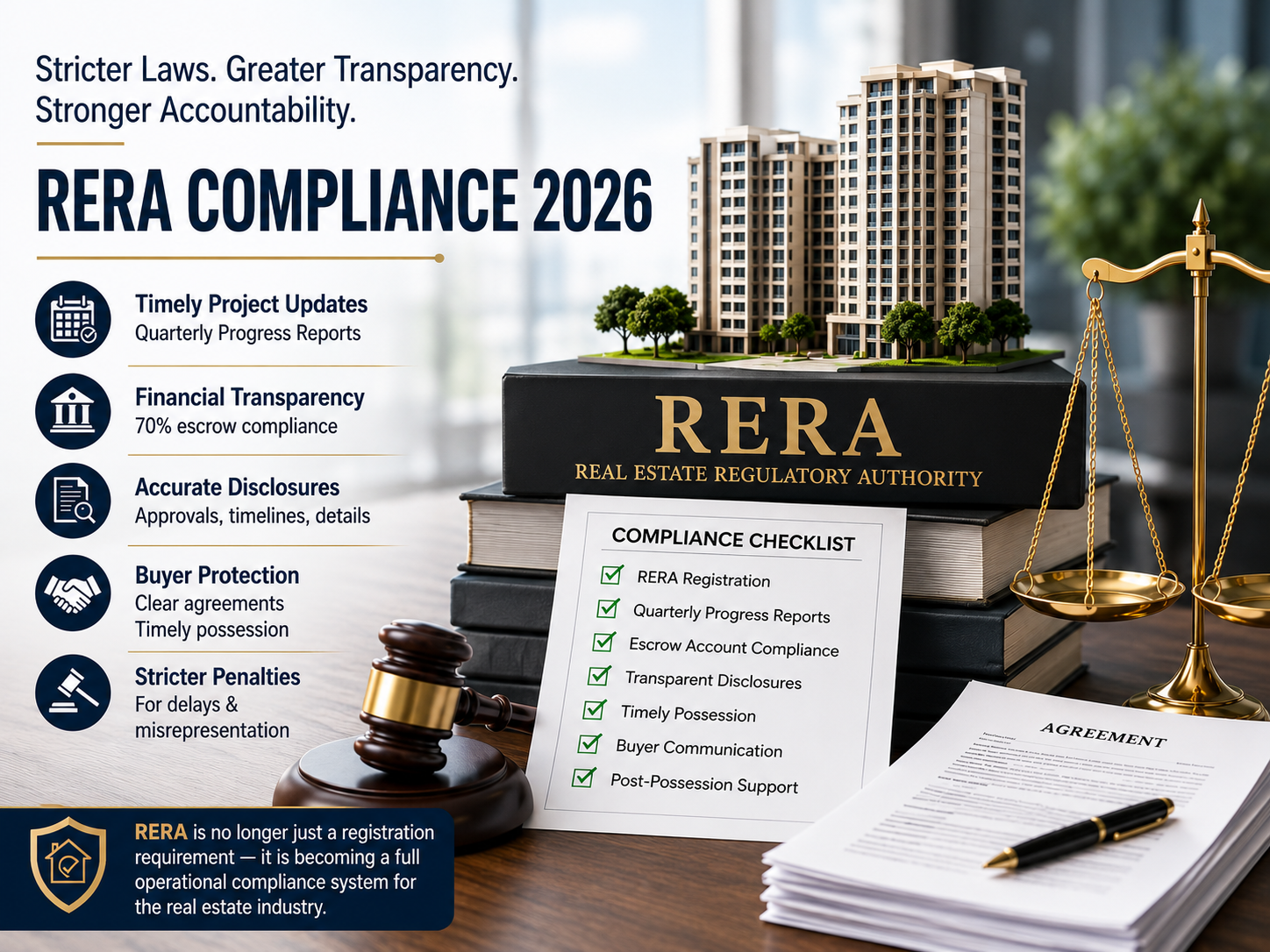

RERA Act

RERA Act Maharashtra

Maharashtra

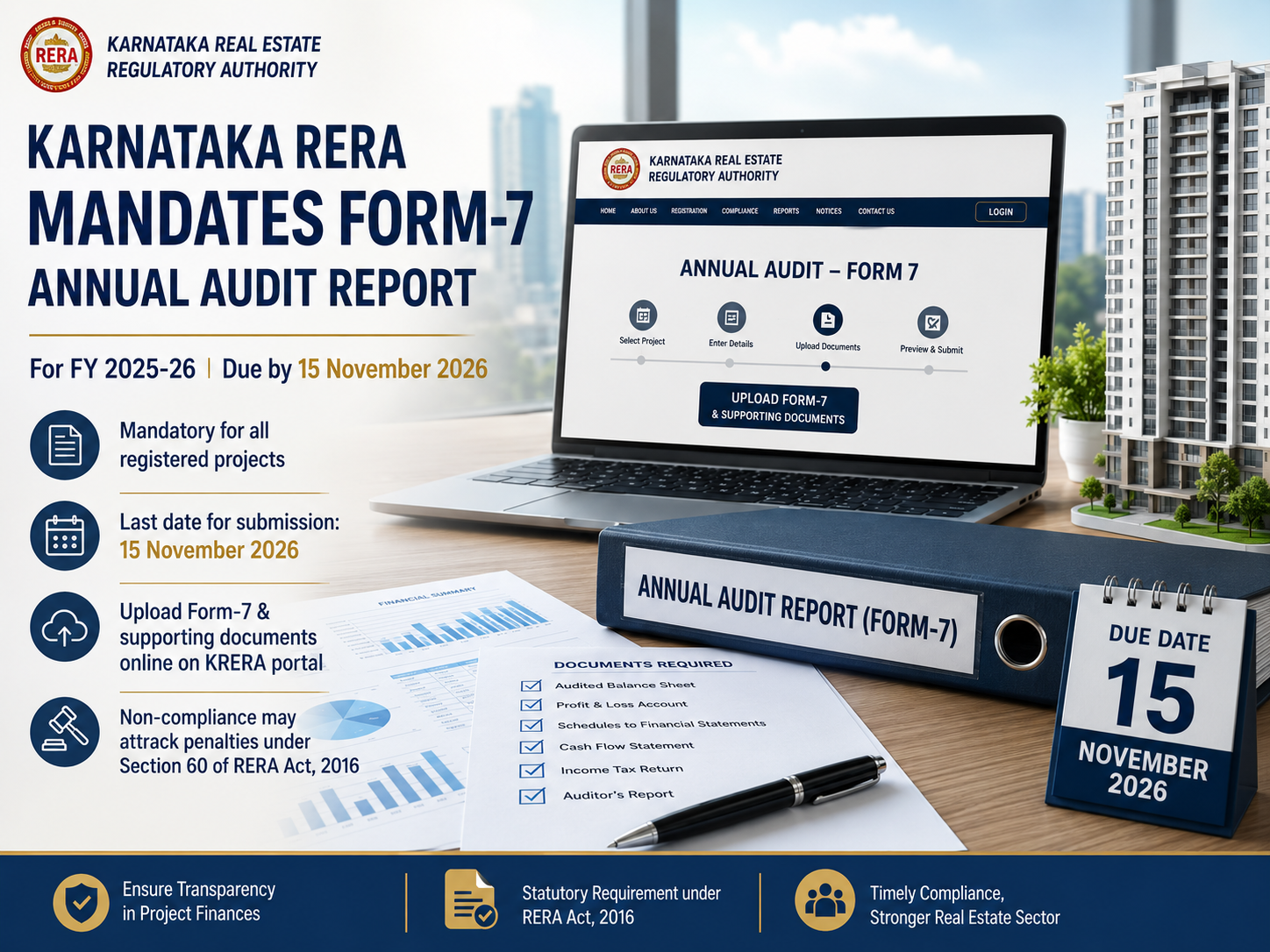

Karnataka

Karnataka

Telangana

Telangana

Andhra Pradesh

Andhra Pradesh

Delhi

Delhi

Uttar Pradesh

Uttar Pradesh

Haryana

Haryana

Gujarat

Gujarat

Bihar

Bihar

- General

- Author: Riya Kapoor

Highlights

-

every promoter is required to open RERA separate account in a scheduled bank to cover the cost of construction and land cost of the project.

-

The basic principle is that only actual out-flows can be charged to the account, not notional values or future payments.

-

Marketing/Advertising costs and loan repayment/interest payments to financial institutions are not permissible to be charged against the 70% of the designated account.

As per section 4(2)(I)D), every promoter is required to open RERA separate account in a scheduled bank to cover the cost of construction and land cost of the project.

The withdrawal from such accounts should be in accordance with acts, rules, and regulations as prescribed. Only certain expenses are charged from a designated bank account.

In the macro sense, only the cost of land and the cost of on-site construction can be charged to the designated account. The basic principle is that only actual out-flows can be charged to the account, not notional values or future payments.Marketing/Advertising costs and loan repayment/interest payments to financial institutions are not permissible to be charged against the 70% of the designated account.

Following are the expenses that can be charged to RERA separate account:-

(A) Land: Actual amount paid for land at the time of purchase (not current notional value, even though this may be used for fixing the price of apartments).If the land is ancestral or received as inheritance or gift, then the permissible charge to the designated account will be nil. In case of JV when landowner is someone other than the promoter, amounts actually paid to the owner of the land are permissible. If payments are made in 2 installments, then the charge to the designated account can be made as and when the payments are actually made. They cannot be frontloaded. Stamp duty, registration costs, and legal fees actually paid for such transactions can also be charged. Amount paid for diversion and/or additional FAR is permissible.

(B) Fees: Fees paid to any statutory authority to obtain project approval or registration (such as fees paid to RERA, Town & Country Planning Deptt., Municipal/Local Authority or Panchayat) may be charged to the account Fees paid to Architect/ Structural Engineer/ Technical Consultant are permissible, provided these are specifically for this project, and these experts are not salaried employees of the Promoter. Only such fees as are directly attributable to the project are permissible.

(C) On-site Construction: Only such payments as are directly related to construction are permissible. The cost of bringing water and electricity to the project site is permissible. The depreciation cost of machinery and equipment used on a project site or hire and maintenance charges for the same is permissible. Consumables, such as diesel, 3 lubricants, etc. and electricity to run the equipment is also permissible. Cost of material actually purchased. The cost of project-related labor actually paid (excluding the cost of salaries of employees of the company) is permissible to be charged to the designated accounts.

So, the above expenses are allowed from RERA separate account. Expenses other than mentioned above will not be charged from the bank account.

In case of any query, you can contact us.

Copyright © 2026 RERA Filing. All rights reserved.