RERA Act

RERA Act Maharashtra

Maharashtra

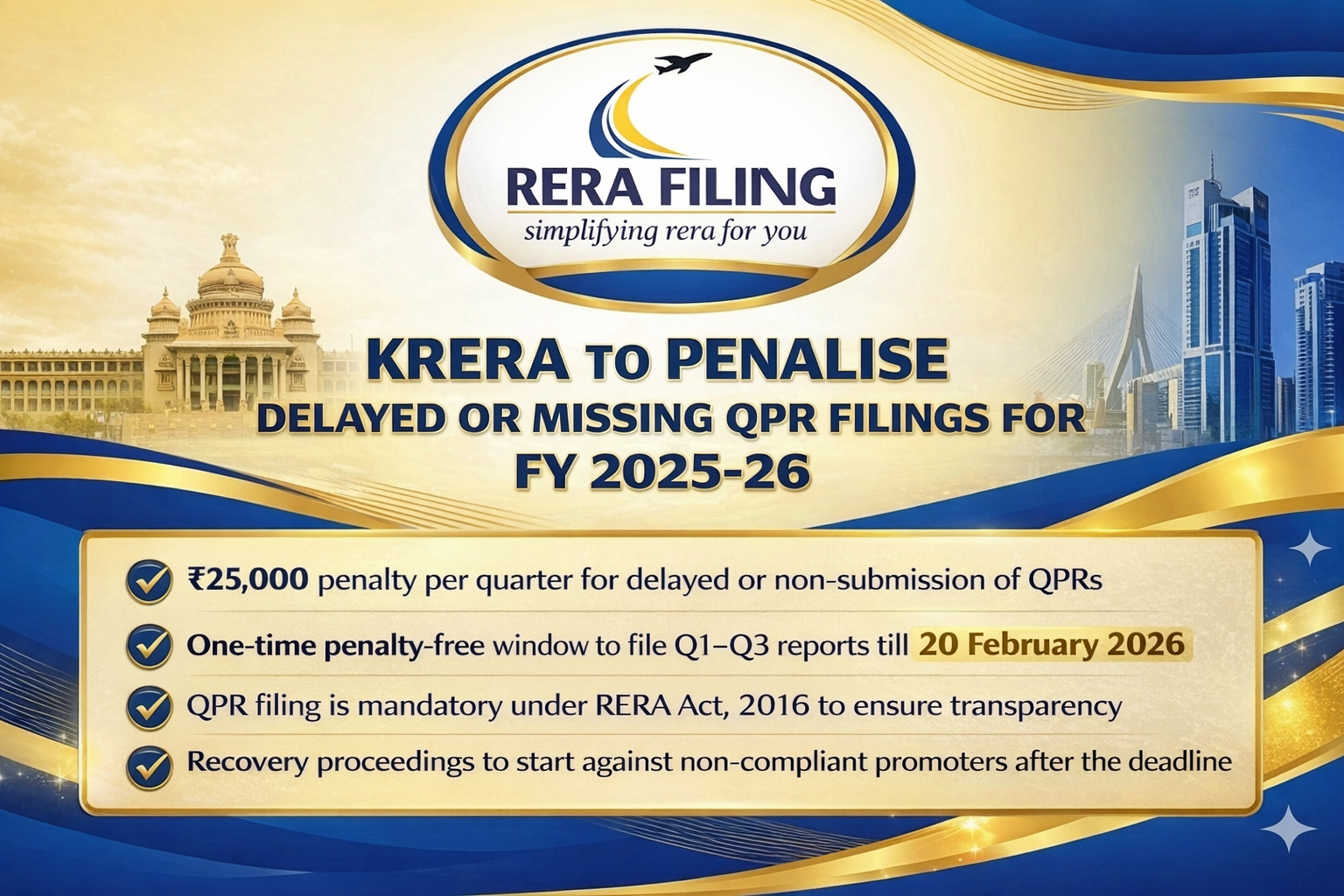

Karnataka

Karnataka

Telangana

Telangana

Andhra Pradesh

Andhra Pradesh

Delhi

Delhi

Uttar Pradesh

Uttar Pradesh

Haryana

Haryana

Gujarat

Gujarat

Bihar

Bihar

- General

- Author: Riya Kapoor

Highlights

-

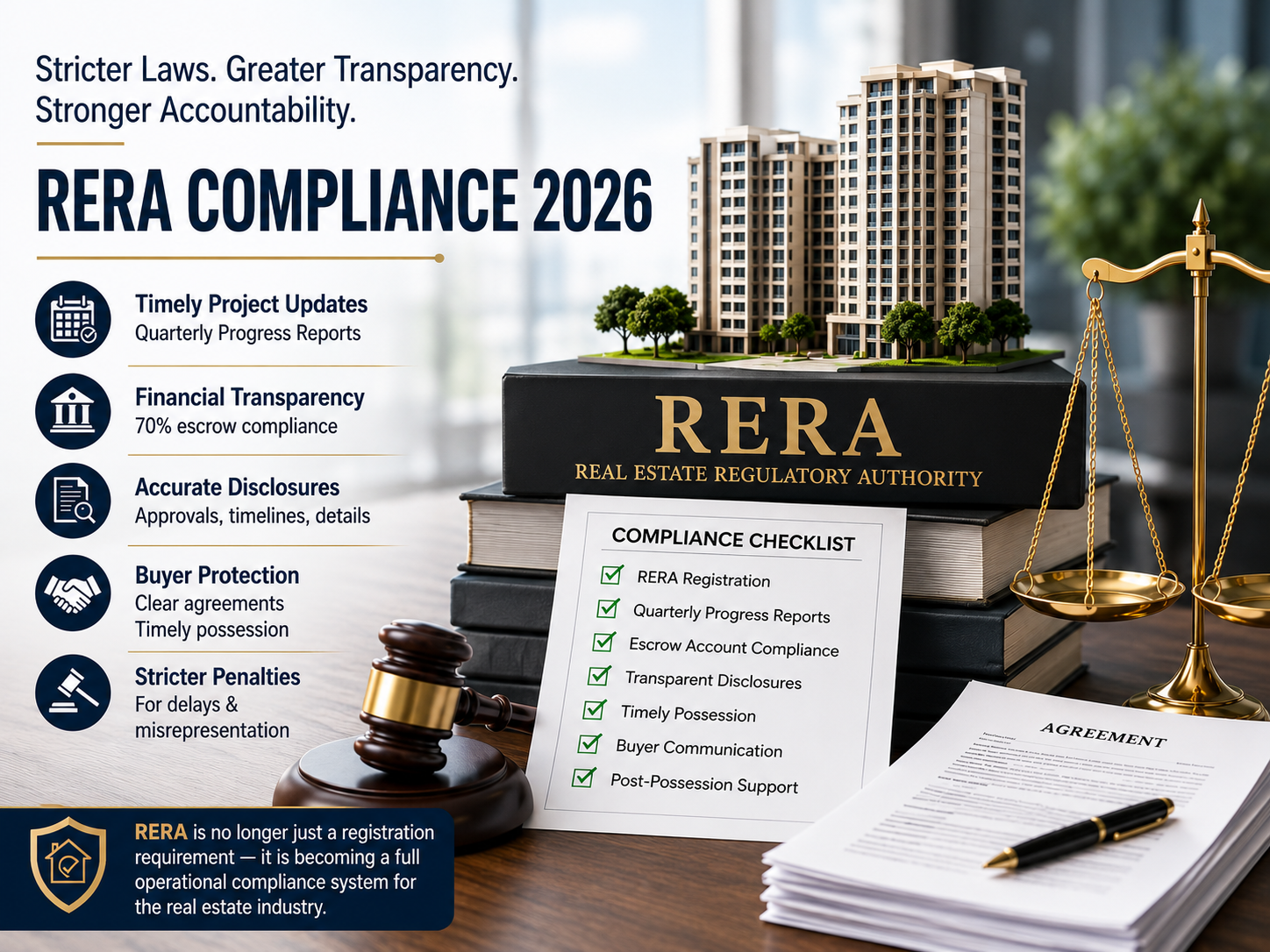

The section 4(l)(D) of RERA, 2016 casts responsibility on the Promoter (builder/developer) to deposit 70% of the amounts realised for the real estate project from the allottees (buyers).

-

The second proviso to section 4(l)(D) prescribes the certificates to be obtained to withdraw funds from the separate account, which includes a certificate to be obtained from a CA.

-

The dawn of RERA has put a halt on the malpractices the builders indulged into.

RERA is one of the most beneficial and exemplary steps taken by the Central Government to the plight of homebuyers. The dawn of RERA has put a halt on the malpractices the builders indulged into. According to Section 4(2) of the RERA, it is mandatory that the amounts from the separate bank account (in which 70% of the amounts realized for the real estate project from the allottees, from time to time to cover the cost of construction and the land cost and shall be used only for that purpose) shall be withdrawn by the promoter after it is certified by professionals.

Provision as per the Law

1.1 The section 4(l)(D) of RERA, 2016 casts responsibility on the Promoter (builder/developer) to deposit 70% of the amounts realised for the real estate project from the allottees (buyers), which can be withdrawn only in proportion of work completed.

1.2 The second proviso to section 4(l)(D) prescribes the certificates to be obtained to withdraw funds from the separate account, which includes a certificate to be obtained from a CA.

1.3 Whereas the third proviso to section 4(2)(1)(D) of RERA further provides that the promoter shall get his accounts audited within six months after the end of every financial year by a chartered accountant in practice, and shall produce a statement of accounts duly certified and signed by such chartered accountant and it shall be verified during the audit that the amounts collected for a particular project have been utilized for the project and the withdrawal has been in compliance with the proportion to the percentage of completion of the project.

Purpose of Forms

Form 3 - Certificate for withdrawal of funds from a separate account. The practicing chartered account will certify the cost incurred on construction cost and the land cost. The CA is also required to certify the proportion of cost incurred on construction and land cost to the total estimated cost of the project.

Form 5- Annual report on the statement of accounts from Statutory auditor. It will certify that amount collected for a particular project has been utilized only for such project and withdrawal has been in compliance with the proportion to the percentage of completion.

Time Interval

Form 3 is required to be submitted at the time of project registration and when promoter wishes to withdraw money from the separate account

Form 5 is an annual report on the statement of accounts within 6 months from the end of the financial year.

Type of CA

Form 3- To be taken from practicing chartered accountant other than the statutory auditor

Form 5- to be taken from Statutory auditor

For any clarification, contact us.

Copyright © 2026 RERA Filing. All rights reserved.